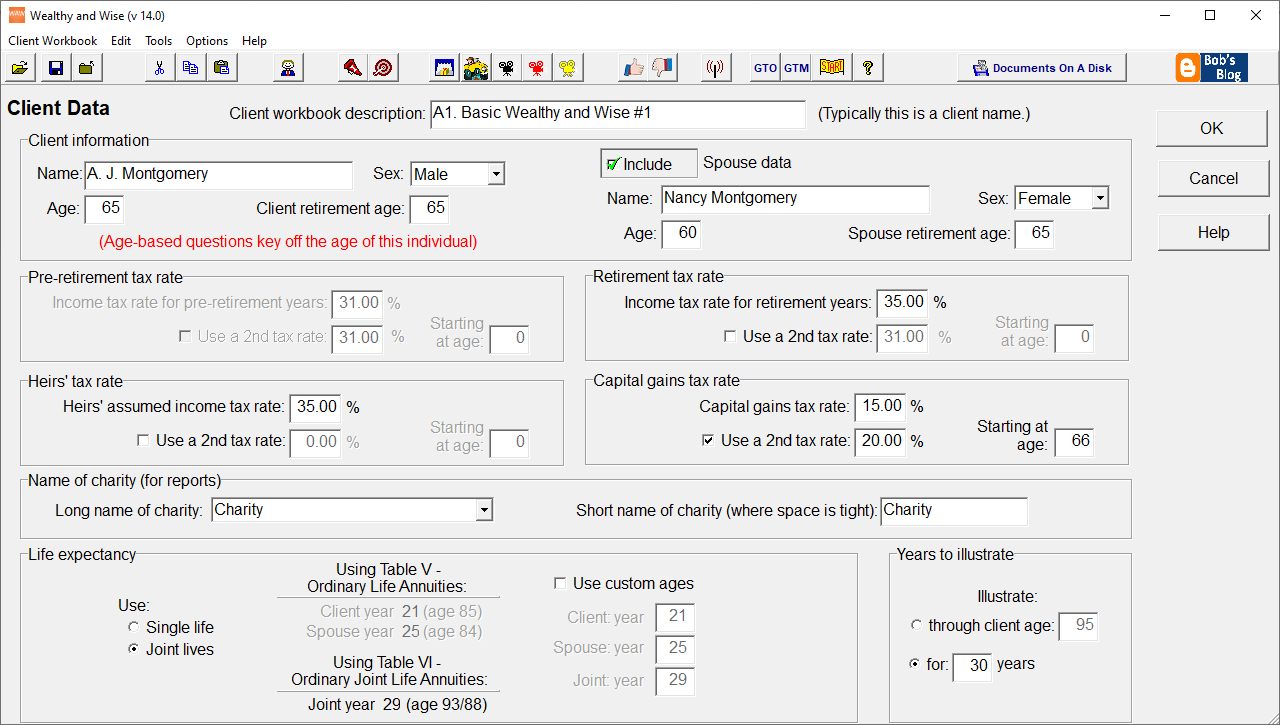

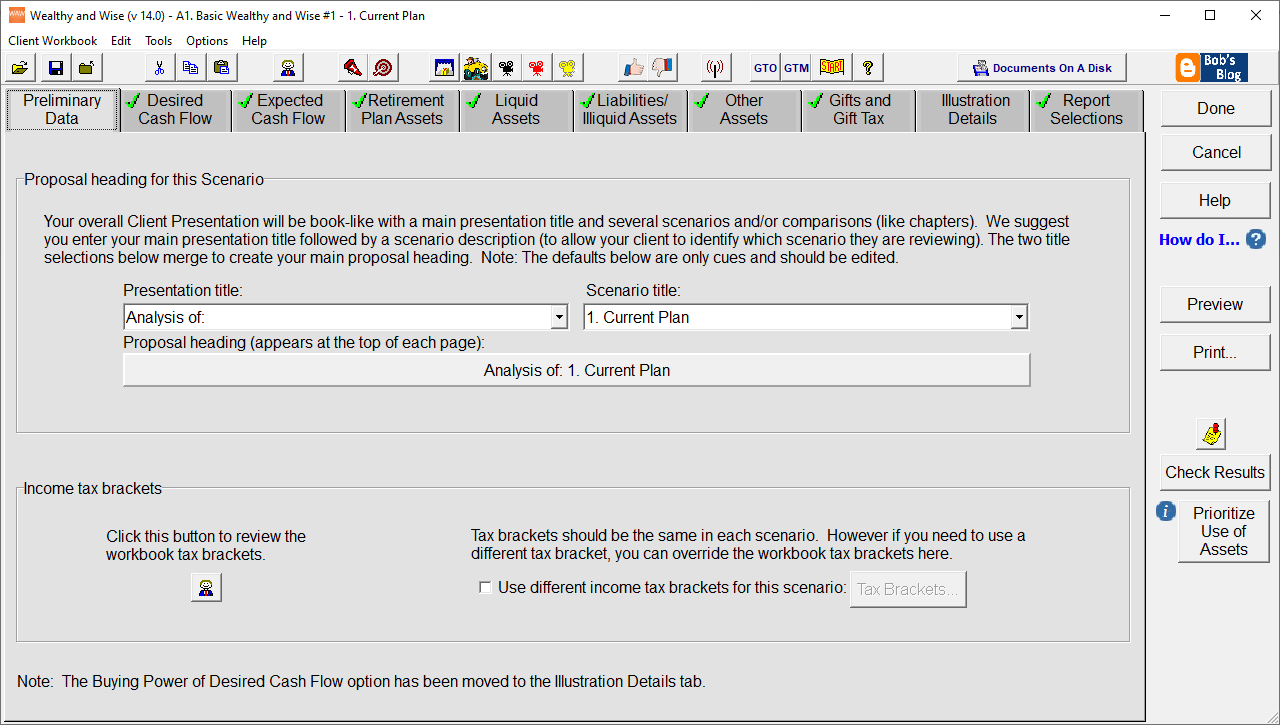

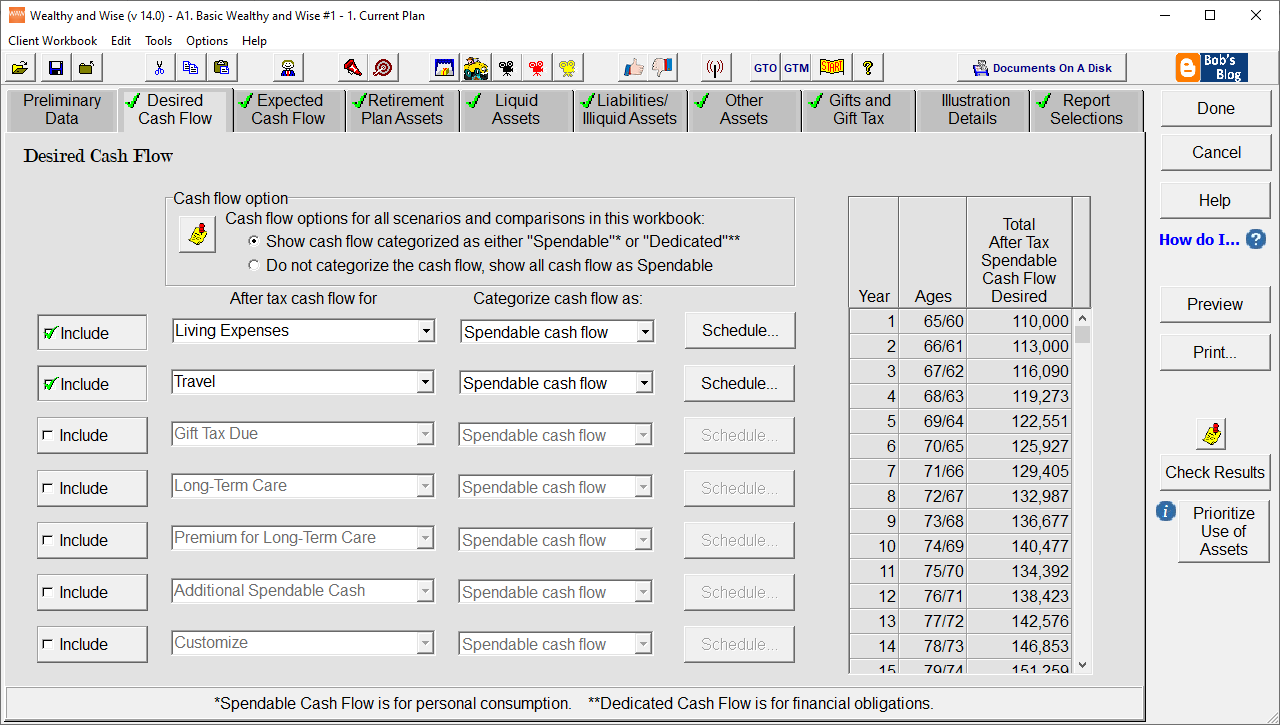

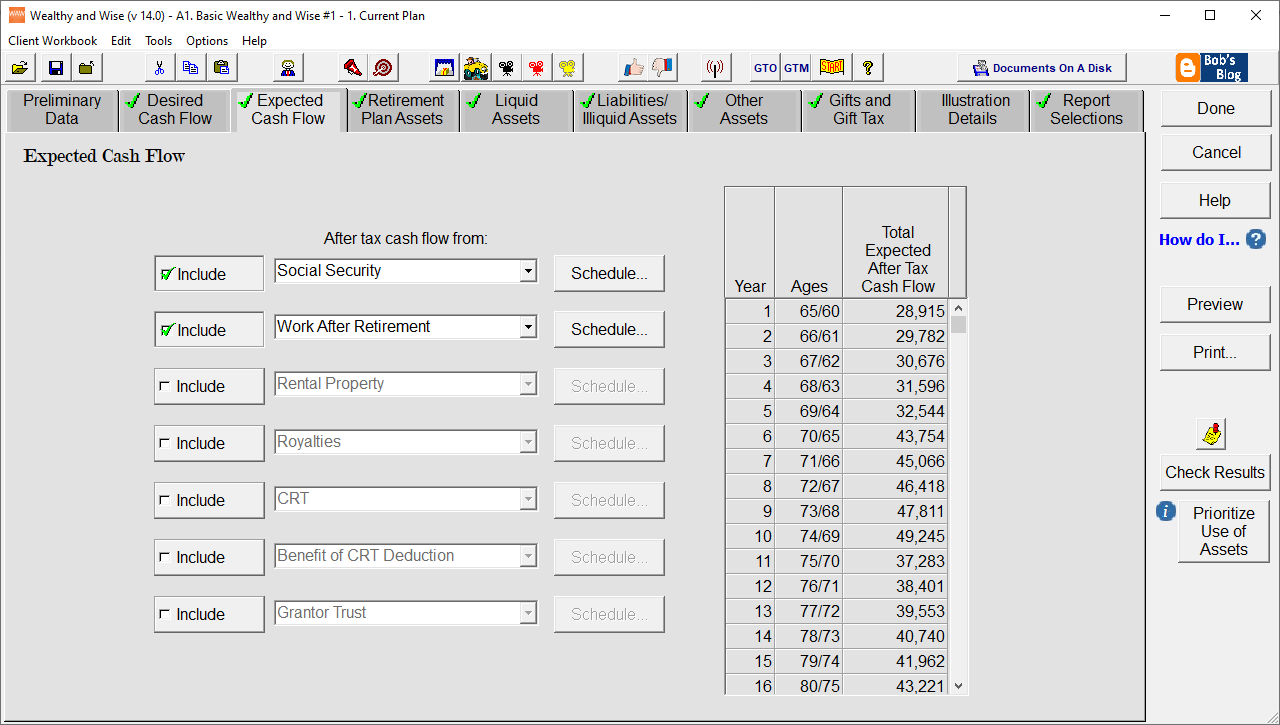

Wealthy and Wise - Sample Input

Premium Financing with Policy Owned by an Irrevocable Trust

Premium Financing with Policy Owned by a Business

Premium Financing with Policy Owned by an Individual

Income Tax Financing with Policy Owned by and Individual Funded by an Employer Bonus

To download a system workbook related to Marketing Alerts, click on the workbook title you want. Be sure to note the directory and path on your hard disk where you have saved the file. Once a workbook file is downloaded, you can import it into the appropriate InsMark System by double clicking on that file name. You can also import it by clicking on Client Workbook/Import Workbook on the Main Toolbar of the appropriate InsMark System and locating the file in the directory where you stored it.

|

Marketing Alert #264

Marketing Alert #263

Marketing Alert #261

Marketing Alert #260

Marketing Alert #259

Marketing Alert #258

Marketing Alert #257

Marketing Alert #256

Marketing Alert #253

Marketing Alert #252

Marketing Alert #249

Marketing Alert #248

Marketing Alert #246

Marketing Alert #243

Marketing Alert #242

Marketing Alert #237

Marketing Alert #234

Marketing Alert #230

Note: This Workbook can be downloaded only after you have installed Version 5.0 of Leveraged Compensation System.

Marketing Alert #227

Marketing Alert #225

Marketing Alert #222

Marketing Alert #220

Marketing Alert #219

Marketing Alert #218

Marketing Alert #217

Marketing Alert #216

Marketing Alert #215

Marketing Alert #213

Marketing Alert #211

Marketing Alert #210

Marketing Alert #209

Marketing Alert #203

Marketing Alert #200

Marketing Alert #199

Marketing Alert #197

Marketing Alert #196

Marketing Alert #193

Marketing Alert #191

Note: This Workbook can be downloaded only after you have installed Version 14.1 of the InsMark Illustration System.

Marketing Alert #189

Marketing Alert #187

Note: This Workbook can be downloaded only after you have installed Version 14.0 of the InsMark Illustration System.

Marketing Alert #186

Note: This Workbook can be downloaded only after you have installed Version 14.0 of the InsMark Illustration System

Marketing Alert #184

Marketing Alert #183

Marketing Alert #175

Marketing Alert #174

Marketing Alert #172

Marketing Alert #171

Marketing Alert #165

Marketing Alert #164

Marketing Alert #163

Marketing Alert #152

|

The name “InsGift -- the Wealthy and Wise System” has been changed to “Wealthy and Wise®”. For some Workbooks, the name “InsGift” may still be referenced. Regardless, they may be imported into Wealthy and Wise.

The name “InsMark Section 7872 Illustration System” has been changed to “Loan-Based Split Dollar System”. For some Workbooks, the name “Section 7872 Illustration System” may still be referenced. Regardless, such Workbooks may be imported into the Loan-Based Split Dollar System.

The name “Leveraged Compensation Plan System” has been changed to “Loan-Based Deferred Compensation System”. For some Workbooks, the name “Leveraged Compensation Plan” may still be referenced. Regardless, such Workbooks may be imported into the Loan-Based Deferred Compensation System.

The insured, age 35, plans on retiring at age 65 and would like to see how life insurance can play an important role in his retirement goals. The policy for this illustration is Universal Life (any permanent policy can be used) with a $250,000 level death benefit. Annual premiums of $3,000 are illustrated for 30 years followed by cash flow of $10,000 a year (withdrawals to basis; loans thereafter) for 20 years. The policy illustration extends to age 95. (Life Plan allows any user-designated final illustration year provided at least two retirement years are included.)

English Version

Spanish Version

The Insured, age 35, plans on retiring at age 65 and would like to see how life insurance can play an important role in his retirement goals. The policy for this illustration is Equity Indexed Universal Life (any permanent policy can be used) with a $500,000 level death benefit. Annual premiums of $6,000 are illustrated for 30 years followed by cash flow of $60,000 a year (withdrawals to basis; loans thereafter) for 20 years. The policy illustration extends to age 95. (Life Plan allows any user-designated final illustration year provided at least two retirement years are included.)

English Version

Spanish Version

An upscale client, age 45, plans on retiring at age 65 and would like to see how life insurance can play an important role in his retirement goals. The policy for this illustration is Equity Indexed Universal Life (any permanent policy can be used) with a $2,500,000 level death benefit. Annual premiums of $100,000 are illustrated for 5 years. Starting at age 65, cash flow of $175,000 a year (withdrawals to basis; loans thereafter) is illustrated for 20 years. The policy illustration extends to age 95. (Life Plan allows any user-designated final illustration year provided at least two retirement years are included.)

English Version

Spanish Version

The illustration below is for the consideration of the wealthy grandparents of a grandchild, age 20. The grandparents would like to provide a head start on retirement planning. The policy for this illustration is Equity Indexed Universal Life (any permanent policy can be used) with a $1,000,000 increasing death benefit (increasing for 10 years, level thereafter). Premiums of $20,000 a year are illustrated for 10 years. Starting at age 55, policy withdrawals of $180,000 a year (withdrawals to basis; loans thereafter) are illustrated for 40 years. The policy illustration extends to age 95. (Life Plan allows any user-designated final illustration year provided at least two retirement years are included.)

View sample output from any illustration proposal below:

Both illustrations reflect a $2,500,000 policy with five $100,000 premiums. The employer provides the insured executive with a bonus of $100,000 for each of the five premiums. The employer also loans the executive an amount equal to the income tax due on each bonus. (Total loans: $40,000 x 5 = $200,000.)

A further bonus is illustrated to provide the executive with the funds for the loan interest due -- resulting in an out-of-pocket cost to the executive of just the income tax on this bonus. (Be sure you examine the Matching Values report for this Sample Illustration as it shows that the executive would have to earn 38.24% in his out-of-pocket cost to match the results of the benefit.)

Note: A gross-up bonus for the loan interest could reduce the executive’s out-of-pocket cost to $0.

The illustration reflects $335,000 in after tax policy cash flow at the beginning of year 21 and $135,000 a year thereafter (after tax cash flow means withdrawals to basis; loans, thereafter). $200,000 of the $335,000 of policy cash flow in year 21 repays the loans from the employer. This leaves $135,000 of after tax policy cash flow in year 21 - along with the $135,000 of after tax policy cash flow in succeeding years -- directed to tax free retirement income for the executive

This illustrates Leveraged Deferred Compensation for an executive of a Profit-Making Organization using a $2,500,000 policy with five $100,000 premiums. The insured executive adjusts his compensation downward by $100,000 a year for five years which covers a major portion of the employer's funding costs. The employer uses the after tax dollars provided by the executive's compensation reduction as part of the funding for the loans to the executive who, in turn, uses the loans for premium payments.

Note: The executive’s compensation adjustment that is retained by the employer adds to the taxable profit of the employer and thus increases the amount of income tax due by the employer. In a 34% employer bracket, for example, $100,000 not paid to the executive produces $66,000 in after tax funds for the employer. Adding $34,000 of employer funds to the $66,000 produces the $100,000 loan to the executive. Reducing cash by $34,000 in this case produces a $100,000 loan receivable for the employer -- a credit to earnings of $66,000 ($100,000 - $34,000).

A gross-up bonus (also known as a "double" bonus) is illustrated to provide the executive with the funds for loan interest payments as well as the tax on the bonus. (This reduces the credit to earnings somewhat.)

The illustration reflects $600,000 in after tax policy cash flow at the beginning of year 21 and $100,000 a year thereafter (after tax cash flow means withdrawals to basis; loans, thereafter). $500,000 of the $600,000 of policy cash flow in year 21 repays the loans from the employer. This leaves $100,000 of after tax policy cash flow in year 21 -- along with the $100,000 of after tax policy cash flow in succeeding years -- directed to tax free retirement income for the executive.

This illustrates Leveraged Deferred Compensation for an executive of a Tax Exempt Organization using a $2,500,000 policy with five $100,000 premiums. The insured executive adjusts his compensation downward by $100,000 a year for five years which covers all of the employer's funding costs. The employer uses the dollars provided by the executive's compensation adjustment for loans to the executive who, in turn, uses the loans for premium payments.

Note: In a Tax Exempt Organization’s 0% tax bracket, $100,000 not paid to the executive produces $100,000 in funds for the employer to loan to the executive. The transaction thus produces a $100,000 in annual loan receivables for the employer resulting in a credit to earnings of $500,000 over five years.

A gross-up bonus (also known as a "double" bonus) is illustrated to provide the executive with the funds for loan interest payments as well as the tax on the bonus. (This reduces the credit to earnings somewhat.)

The illustration reflects $600,000 in after tax policy cash flow at the beginning of year 21 and $100,000 a year thereafter (after tax cash flow means withdrawals to basis; loans, thereafter). $500,000 of the $600,000 of policy cash flow in year 21 repays the loans from the employer. This leaves $100,000 of after tax policy cash flow in year 21 -- along with the $100,000 of after tax policy cash flow in succeeding years -- directed to tax free retirement income for the executive.

Note: Sample Leveraged Deferred Compensation Illustrations involving the use of an additional severance benefit are included in the Sample Illustration section of the Leveraged Compensation System.

This illustrates Leveraged 401(k) Look-Alike for an executive of a Profit-Making Organization using a $2,500,000 policy with five $100,000 premiums. The insured executive adjusts his compensation downward by $100,000 a year for five years which covers a major portion of the employer's funding costs. The employer uses the after tax dollars provided by the executive's compensation reduction as part of the funding for the loans to the executive who, in turn, uses the loans for premium payments.

Note: The executive’s compensation adjustment that is retained by the employer adds to the taxable profit of the employer and thus increases the amount of income tax due by the employer. In a 34% employer bracket, for example, $100,000 not paid to the executive produces $66,000 in after tax funds for the employer. Adding $34,000 of employer funds to the $66,000 produces the $100,000 loan to the executive. Reducing cash by $34,000 in this case produces a $100,000 loan receivable for the employer -- a credit to earnings of $66,000 ($100,000 - $34,000).

A gross-up bonus (also known as a "double" bonus) is illustrated to provide the executive with the funds for loan interest payments as well as the tax on the bonus. (This reduces the credit to earnings somewhat.)

The illustration reflects $600,000 in after tax policy cash flow at the beginning of year 21 and $100,000 a year thereafter (after tax cash flow means withdrawals to basis; loans, thereafter). $500,000 of the $600,000 of policy cash flow in year 21 repays the loans from the employer. This leaves $100,000 of after tax policy cash flow in year 21 -- along with the $100,000 of after tax policy cash flow in succeeding years -- directed to tax free retirement income for the executive.

This illustrates Leveraged 401(k) Look-Alike for an executive of a Tax Exempt Organization using a $2,500,000 policy with five $100,000 premiums. The insured executive adjusts his compensation downward by $100,000 a year for five years which covers all of the employer's funding costs. The employer uses the dollars provided by the executive's compensation adjustment for loans to the executive who, in turn, uses the loans for premium payments.

Note: In a Tax Exempt Organization’s 0% tax bracket, $100,000 not paid to the executive produces $100,000 in funds for the employer to loan to the executive. The transaction thus produces a $100,000 in annual loan receivables for the employer resulting in a credit to earnings of a $500,000 over five years.

A gross-up bonus (also known as a "double" bonus) is illustrated to provide the executive with the funds for loan interest payments as well as the tax on the bonus. (This reduces the credit to earnings somewhat.)

The illustration reflects $600,000 in after tax policy cash flow at the beginning of year 21 and $100,000 a year thereafter (after tax cash flow means withdrawals to basis; loans, thereafter). $500,000 of the $600,000 of policy cash flow in year 21 repays the loans from the employer. This leaves $100,000 of after tax policy cash flow in year 21 -- along with the $100,000 of after tax policy cash flow in succeeding years -- directed to tax free retirement income for the executive.

Any of the above illustration concepts are superior to classic uses of Deferred Compensation or Salary Continuation arrangements due to the fact that the participating executive has a personally owned policy from which tax free retirement cash flow can be provided through tax free policy loans.

Candidates for these plans are key employees that the business believes deserve a special executive benefit. Any of the plans should also work well for employee shareholders and non-shareholder key employees of C corporations and non-owner employees of all other business entities including tax exempt organizations (the latter being a rich source of prospects for the concept).

© 2026 InsMark LLC All Rights Reserved.